View SMM spot aluminum quotes, data, and market analysis

Order and view SMM metal spot historical price trends

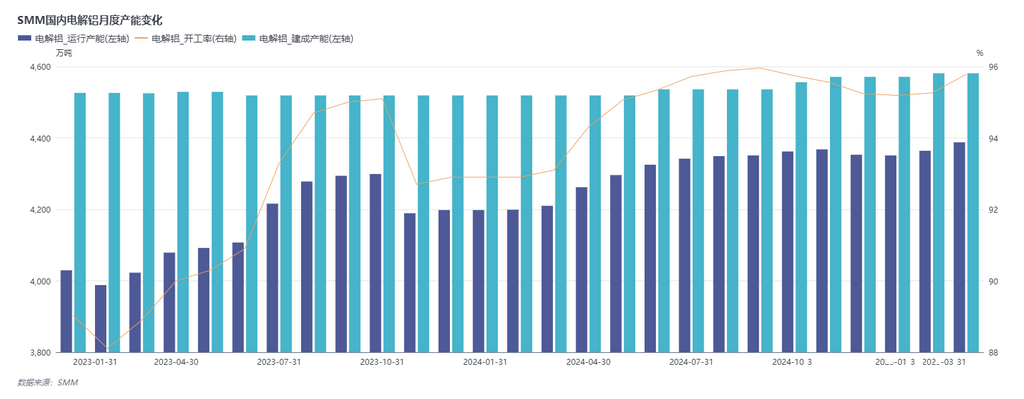

SMM March 31 news:

According to SMM statistics, domestic aluminum production in March 2025 (31 days) increased by 3.7% YoY and 11.2% MoM. Domestic aluminum operating capacity rose MoM, mainly due to the gradual resumption of production at aluminum smelters, with some resumptions in February already yielding output. The proportion of liquid aluminum at domestic aluminum smelters rebounded to normal levels, with the industry's liquid aluminum ratio increasing by 3.2 percentage points MoM and 0.15 percentage points YoY to 74.2%. Additionally, recent losses at downstream billet plants in Guangxi led to production cuts, causing a decline in the liquid aluminum ratio at some local smelters by month-end. Based on SMM's liquid aluminum ratio data, domestic aluminum casting ingot production in March increased by 3.1% YoY to around 958,000 mt.

Capacity changes: As of the end of March, SMM statistics show that domestic aluminum existing capacity was approximately 45.81 million mt, with operating capacity around 43.88 million mt. The industry's operating rate rose by 0.5 percentage points MoM and 2.8 percentage points YoY to 95.8%. Currently, aluminum smelters in Sichuan and Chongqing have largely resumed production, while a Guangxi smelter undergoing technological transformation is expected to resume production around October 2025, and another previously loss-making smelter in Guangxi has already resumed production. Additionally, a smelter in Qinghai has started production after a replacement and upgrade project, contributing to future growth in aluminum operating capacity.

Production forecast: Entering April 2025, domestic aluminum operating capacity is expected to rise again as related companies start production and reach full capacity. By the end of April, domestic annualized aluminum operating capacity is projected to slightly increase to 43.92 million mt/year. Aluminum prices continue to fluctuate at highs, while downstream demand is expected to rise as the peak season begins. However, with end-users pushing for lower prices, processing fees for aluminum billets and others have declined, and losses at billet plants in Guangxi have led to renewed production cuts. The liquid aluminum ratio in April may see a slight correction to around 73%. Continued attention is needed on the resumption of aluminum capacity across regions and the operating rates of downstream liquid aluminum products such as billets.